11.21.2025

Sausage casings bulletin, November 21, 2025

...

Last week the US hide market continued under pressure with some buyers testing the market with aggressive low bidding while some stood on the sidelines waiting to see what happens. The pressure was on suppliers to find a level that buyers would step forward and enter the market, especially considering large slaughter numbers coming for summer grilling season. Prices were mixed with trading generally around a dollar or so lower, but a few small volume sales sold closer to steady. Included were HTS sold for $67 to $68, HNS sold from $73 to $75 and BBS from $72 to $73. The Jacobsen Hide Index closed the week on Thursday at $64.85 from $65.36 a week ago. A number people in the hide industry opined that producers will continue pushing for sales on most selections this week.

Meanwhile, in China the government held a video conference on April 5 about environmental inspection on polluting industries that could affect the tanning industry. The ministry of environmental protection will start the largest one-year supervision in history, involving 5600 environment law enforcement officers, covering Beijing, Tianjin, Hebei and surrounding 18 cities. It is understood that this strengthened supervision is the biggest action directly organized by national department in environmental protection history.

Today’s Market

The market began the week on a quiet note with only one packer quote for HTS at $67. While a couple suppliers indicated they did a decent amount of business, the feeling was that not all of last week’s hides were sold; however, this will need to be confirmed.

HTS 62/64 @ $67.00

No processor sales today.

Cattle/Beef: Demand Strength Seen Across the Cattle Complex

Thus far in 2017, a larger portion of U.S. winter wheat area was under moderate or more intense drought conditions than in 2016. Along with lower prices for wheat, the situation likely provides an option for producers to graze-out wheat pastures for backgrounding. To the extent that demand for calves to graze out these areas increases, prices of lighter-weight calves may find support. However, the timing of movement of these calves off pasture and into feedlots will likely impact both the level of placements and the price of heavier-weight calves in the coming months.

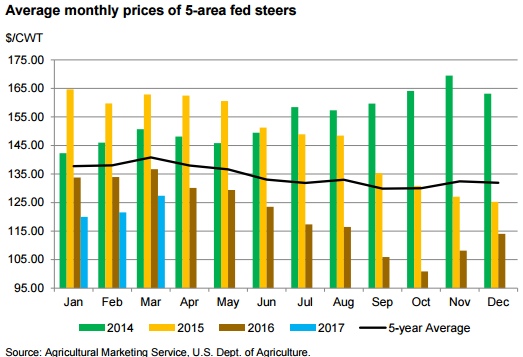

Feeder and fed cattle prices were supported by relatively strong demand during the first quarter, but packer demand has likely weakened as margins have been squeezed by weakening wholesale prices. The timing of beef sales ahead of grilling season may influence packer demand during the quarter, but second-quarter steer and heifer slaughter will likely reflect the marketing of the large number of cattle placed on feed in late 2016. Weekly dressed weights for cattle during March were slightly higher than previously expected and second quarter carcass weights were raised, helping to support an increased forecast of commercial beef production in the first half of 2017.

Wholesale beef cutout values strengthened toward the end of the first quarter; however, this is not surprising, given the tendency for both Choice and Select beef cutouts to gain momentum heading into the spring grilling season, when the market transitions from lower-valued end cuts to more expensive middle meat cuts. The weekly boxed beef cutout data (USDA AMS report LM_XB459) reports choice cutout values that advanced from mid-February’s low of $188.93 to $223.12 per cwt on March 24, with Select cutout values also gaining impressively over the period. However, wholesale beef prices have declined since the last week of March.

The gains in the boxed beef cutout values through late-March are the result of significant gains in beef middle meats (i.e., the rib and loin primals). However, boxed beef cutout values began showing signs of weakness in late-March, squeezing packer margins and likely pressuring fed cattle prices. The first quarter 5-area weighted steer price averaged $122.96 per cwt. The 5-area weekly weighted steer price has weakened from $127.38 during the last week of March to $124.33 per cwt in early April. Beef packers appear to be backing off recent higher prices for fed cattle. Fed steer prices reached $132 per cwt in the third week of March before declining to average $124 per cwt in the first week of April. Fed cattle prices in the second quarter are forecast to average $117-$121 per cwt, pressured by large supplies of cattle available for slaughter from late-2016 and early-2017 feedlot placements.

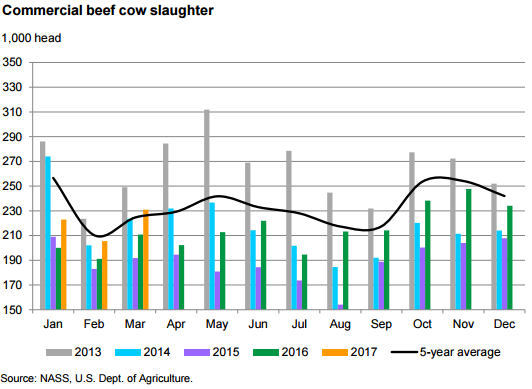

Estimated federally inspected weekly total cow slaughter for the first quarter was up about 5% compared to the same period in 2016. Beef cow slaughter is almost 10% higher year-over-year. However, cow slaughter as a proportion of the January 1 beef cow herd is only slightly higher than 2016, but below the average for 2012-2016, a period which included drought-induced liquidation. First-quarter prices for cutter cows were estimated at $62.63 per cwt, and prices for the remaining quarters for 2017 are likely to tick higher. Second-quarter cutter cow prices are forecast to average $63-$66 per cwt.

Mexican Feeder Cattle Imports Continue to Show Strength

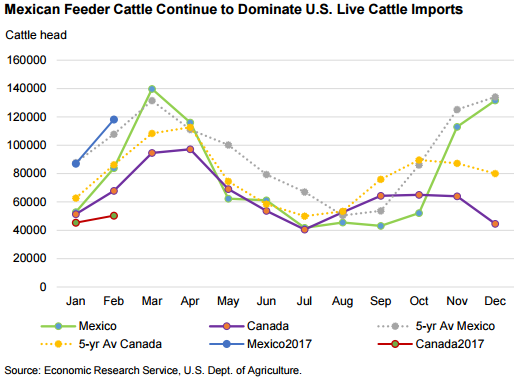

In February 2017, U.S. live cattle imports increased by 27% from the previous month to 168,473 head, 11% up from the same period a year ago. More than 85% of the feeder cattle imported from Mexico were in the 400- to 700-pound weight range, while almost all the feeder cattle imported from Canada were over 700 pounds. For most of 2016, there was not a large difference between the number of cattle imported from Mexico and Canada but since November 2016, live cattle imports from Mexico have been significantly higher than imports from Canada. January and February imports from Mexico were above the 5-year average, while imports from Canada were below it. The strength of the U.S. Dollar relative to the Mexican Peso and a rebuilding of the Mexican herd are likely contributing factors to this uptick in imports from Mexico.

In February 2017, U.S. live cattle exports were up 66% from a year ago to 8,299 head; however, volume was down 36% from January. Mexico and Canada were the primary export destinations, responsible for 80% of total U.S. live cattle exports. February U.S. live cattle exports to Mexico declined sharply (69%) from the previous month to 1,049 head, 57% lower than the same month a year ago.

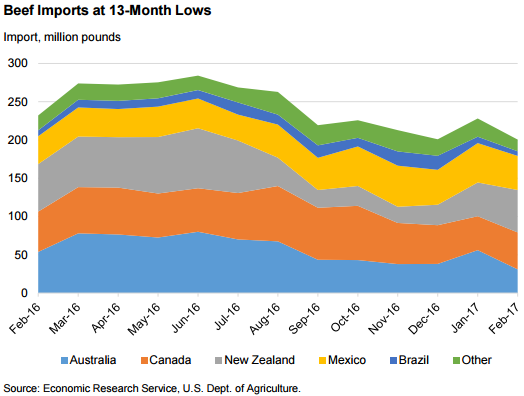

U.S. Beef Imports Expected to Decline in First Quarter 2017

In February 2017, the United States imported 200.5 million pounds of beef 14% below a year ago. This is likely due to lower supplies in several key importing countries coupled relatively large supplies of processing-grade beef in the United States. New Zealand, Canada, Mexico, Australia, and Nicaragua were the top five suppliers, accounting for 93% of total U.S. beef imports in February 2017. U.S. imports from Australia declined 42% from year-earlier levels, likely due to continuing herd rebuilding in Australia. Imports from Canada also declined by 9% to 6 million pounds in February from the previous month, and imports from New Zealand declined by 11% to 44.5 million pounds from last year. Some of the declines were offset by 22% higher imports from Mexico. First-quarter 2017 U.S. beef imports are estimated at 685 million pounds, a 14% year-over-year decline.

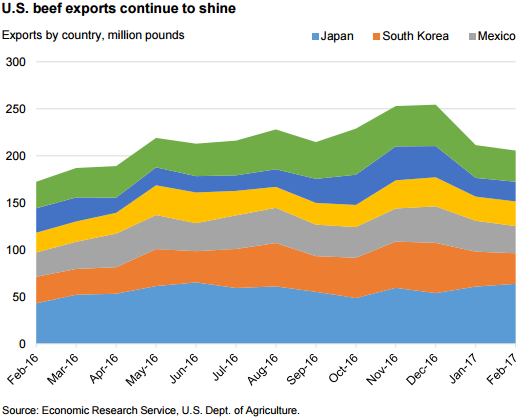

Lower U.S. Beef Prices Bolster Year-Over-Year Increase in Exports

U.S. beef exports more competitive. In February 2017, U.S. beef exports increased by 19.3% from the same period a year ago to 205.5 million pounds. The United States exported about 84% of February’s volume to Japan, South Korea, Mexico, Canada, and Hong Kong. Each market saw double-digit percentage-point increases year-over-year for February except for Hong Kong, which imported 19.2% less.

Link to complete USDA report: LIVESTOCK, DAIRY, & POULTRY OUTLOOK

Apr 17 (Business-Standard) INDIA — Shifting of Tanneries: Kanpur Exporters Losing Business to Pakistan

The ban on slaughterhouses and the proposed shifting of tanneries from Kanpur in name of cleaning the Ganga is hampering leather exports from the country, with enterprises in Kanpur losing business to their competitors in Pakistan. The recent crisis in the leather industry is steadily impacting the Rs 6,000 crore annual export business from the city, and exporters based there estimate that at least 50 per cent of their export business has already gone to Pakistan. READ MORE

Apr 16 (Korean Herald) KOREA — Korean Automakers’ Domestic Sales Exceed W40tr for First Time

Domestic sales of Korea’s top five local automakers surpassed 40 trillion won ($35.2 billion) for the first time last year, according to industry reports Sunday. Local carmakers including Hyundai Motor, Kia Motors, Korea GM, Renault Samsung, and SsangYong Motor posted domestic sales of roughly 41.17 trillion won last year, a 7.7 percent on-year jump compared to 2015. READ MORE

Apr 16 (Dhaka Tribune) BANGLADESH — Tanners Fear Cancellation of Huge Export Orders

Leather factory owners are fearing the loss of export orders following the shutdown of Hazaribagh tanneries over their failure to relocate to Savar Tannery Estate. The tanners who have already shifted their units to the Savar estate are also facing the same threat as they are yet to install their crust and finished leather sections as the gas connection is still not available there. READ MORE

Apr 15 (Detroit Free Press) US — Automakers Voice Opposition to Republican Border Adjustment Tax Plan

“This raising taxes to lower taxes just should not be done,” John Bozzella, president and CEO of Global Automakers said of the proposed border adjustment tax The automotive industry made it clear last week that it is strongly opposed to any proposal to adopt a border adjustment tax, saying it would raise the cost of cars and hurt both the industry and customers. READ MORE

Apr 15 (Daily Nation) KENYA — Firms Stare at Losses as Leather Park Takes Shape

Mixed reactions have greeted the government-backed Sh10 billion Leather Industrial Park, with handicraft makers saying it could push them out of business. The Kinanie Leather Industrial Park Project, a flagship Jubilee initiative, has attracted interest from multinational firms dealing in processing and manufacture of leather goods that will enjoy direct, tax-free entry into Kenya. The 500-acre park, to be granted export processing zone status, is expected to revolutionalise the leather value chain, creating a new market for skins and hides usually processed into blue leather and exported as raw materials. READ MORE

Apr 15 (Business-Standard) INDIA — Worldwide Leather Exports Reports Standalone Net Loss of Rs 0.57 Crore in the March 2017 Quarter

Net Loss of Worldwide Leather Exports reported to Rs 0.57 crore in the quarter ended March 2017 as against net loss of Rs 0.01 crore during the previous quarter ended March 2016. Sales declined 75.93% to Rs 0.26 crore in the quarter ended March 2017 as against Rs 1.08 crore during the previous quarter ended March 2016. READ MORE

Apr 13 (International Leather Maker) BRAZIL — Brazilian Hide Exports Recover from February Fall

Brazil’s hide sector registered an export value of US$192.6 million in the month of March 2017, up 3.8% year-on-year (March 2016: US$ 185.6). According to the Hides and Skins Exports released by SECEX, Brazil’s Foreign Trade Secretariat, March’s figures are 19.5% higher over the previous month of February, when total hide exports amounted to US$ 161.2 million. READ MORE

Apr 13 (International Leather Maker) VIETNAM — Vietnam to Speed up Leather and Footwear Sector Development

Vietnam’s Ministry of Industry and Trade has announced a revised plan for the development of the country’s leather and footwear industry during a seminar held on April 7 in Ho Chi Minh City, Vietnam. Under the revised plan announced by the Government, Vietnam aims to earn between US$24-26 billion from leather and footwear exports by 2020, according to local media reports. READ MORE

11.21.2025

Sausage casings bulletin, November 21, 2025

11.14.2025

Sausage casings bulletin, November 14, 2025

11.07.2025

Sausage casings bulletin, November 7, 2025